KARACHI: Pakistan’s gold market continues to experience sharp volatility and little sign of stabilization, with traders and analysts attributing the turbulence to a complex mix of global and domestic factors — from fluctuating international bullion prices and geopolitical tensions to erratic local policies and rupee depreciation.

Experts say the local gold trade remains largely informal and self-regulated, with no credible consolidated data available on market size, demand, or price movements. Institutions like the State Bank, finance and commerce ministries, and the Pakistan Bureau of Statistics hold only partial information, while daily price announcements by gold merchants’ associations often reflect sentiment rather than supply-and-demand dynamics.

Read More: Gold prices drop in Pakistan amid global market weakness

Gold prices have soared dramatically over the past two decades — from around Rs5,000 per 10 grams in 2001 to over Rs350,000 today — marking a 70-fold surge. Despite such gains, returns from real estate and stocks have outperformed gold over the same period. However, in the face of inflation and currency depreciation, many Pakistanis now view gold less as jewelry and more as a secure investment hedge.

Last month, the price of 10 grams of gold swung within a massive Rs58,900 band, peaking at Rs402,100 on October 17 before closing at Rs361,800. Analysts attribute this instability to global bullion trends — including US interest rate policies, central-bank gold purchases, and ETF flows — as well as local pressures like rupee-dollar fluctuations, import bans, smuggling, and seasonal wedding demand.

An All Pakistan Gems and Jewellers Sarafa Association (APGJSA) leader warned that further bouts of volatility are likely due to “external shocks, foreign exchange instability, and informal trade.” Government officials privately confirmed that the temporary gold import and export ban imposed in May — after heightened border tensions with India — was lifted in October under pressure from jewellers and investors.

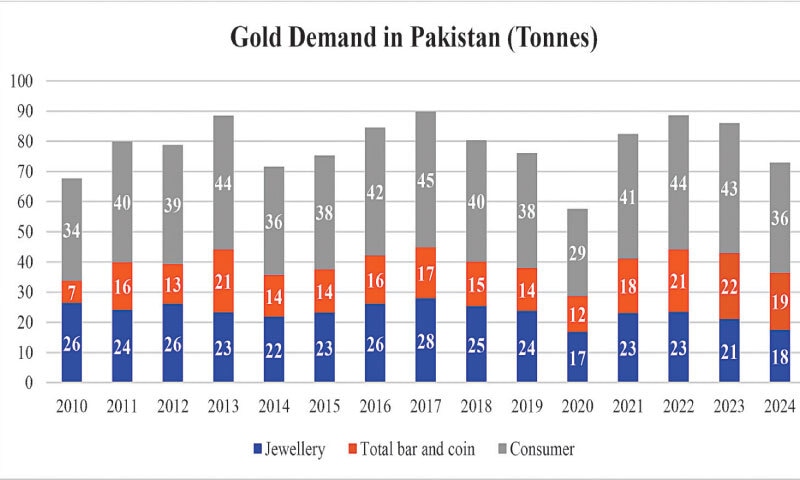

According to the World Gold Council, Pakistan’s gold demand has ranged between 60 and 90 tonnes in recent years, with investment demand rising steadily from 11pc in 2010 to 26pc in 2024. Jewellery consumption, once dominant, now accounts for roughly 24-39pc of total demand, reflecting a broader shift toward gold as a financial safeguard.

Read More: Gold price dips by Rs 1,600 a tola

Officials from the State Bank and the statistics bureau acknowledged that reliable figures on gold holdings and trade remain elusive, with underreporting and informal transactions clouding the true picture of Pakistan’s bullion economy.